The U.S. Treasury Building in Washington, D.C. — now responsible for managing America’s $1.7 trillion student debt portfolio

The biggest shake-up in student loan history just began

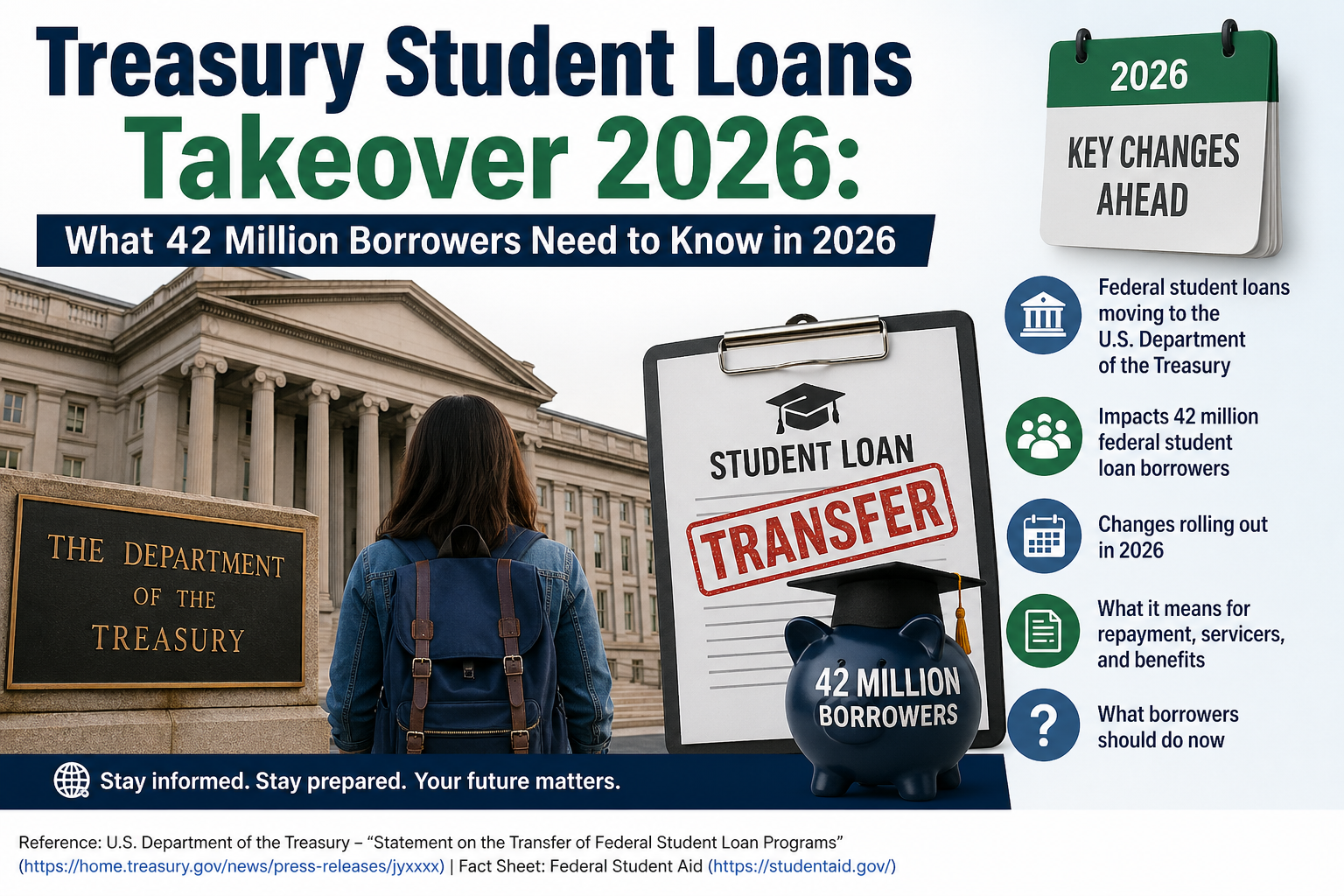

Treasury student loans takeover 2026 For more than four decades, the U.S. Department of Education has been the keeper of America’s federal student loan system — a sprawling, $1.7 trillion portfolio touching the financial lives of over 42 million Americans. That era is ending.

On March 19, 2026, the Trump administration announced a landmark interagency agreement: the Treasury Department will take over management of the federal student loan portfolio in a three-phase transfer that will ultimately strip the Education Department of one of its core functions. It is the most consequential step yet in the administration’s push to shut down the Education Department entirely — a goal that requires an act of Congress, but is already being chipped away at through executive action.

For most borrowers making regular payments, the announcement came with a quick reassurance: nothing changes right now. But for the roughly 11.6 million Americans in default or late-stage delinquency, the shift is immediate — and the stakes couldn’t be higher.

Why now? The numbers behind the crisis

The case for change, at least as the administration frames it, starts with a set of alarming statistics. Fewer than 40% of federal student loan borrowers are currently in active repayment. Nearly one in four — approximately 25% — are in default. And the portfolio itself has ballooned from $1 trillion in 2019 to $1.7 trillion today, a figure twice the size of all U.S. university endowments combined.

Education Secretary Linda McMahon put it bluntly in her announcement statement: “The Department of Education was never intended to operate what would be the fifth-largest commercial bank in the United States.” She argued that the department had “failed to effectively manage and deliver these critical programs” and that borrowers, students, and taxpayers deserve better. Treasury Secretary Scott Bessent echoed the sentiment, calling the move an effort to “clean up a $1.7 trillion portfolio that has been badly mismanaged for years,” and arguing that Treasury has “the unique experience, the operational capability, and the financial expertise to bring long overdue financial discipline to the program.” Critics, including Democratic senators and labor groups, see it differently — calling the transfer an “unlawful dismantling” of a federal agency and warning it will create confusion and chaos for millions of borrowers already struggling to navigate the system.

What the three-phase plan actually looks like

The 17-page interagency agreement outlines a staged handoff, starting with the most financially vulnerable borrowers and expanding outward.

Phase 1: Defaulted borrowers (now underway)

The first phase — already in effect — moves responsibility for approximately 9.2 million borrowers currently in default, plus another 2.4 million in late-stage delinquency, to Treasury’s Bureau of the Fiscal Service. These defaulted loans add up to roughly $180 billion, or about 11% of the total portfolio. Treasury will now manage collections and work to bring these borrowers back into repayment.

Phase 2: Non-defaulted loans (timeline unclear)

The second phase calls for Treasury to “assume operational responsibility” over non-defaulted federal student loans — the remaining $1.5 trillion or so — “to the extent practicable.” No firm timeline has been set for this phase. Its success will largely depend on how well borrowers adapt to the new Repayment Assistance Plan (RAP), which takes effect July 1, 2026.

Phase 3: Full portfolio and FSA functions

Eventually, Treasury is intended to take on all Federal Student Aid functions, including aid disbursement and program administration. This phase has no stated deadline and remains the most politically and legally uncertain of the three.

What this means if you’re a borrower

The administration has been at pains to reassure borrowers that the transfer should be invisible to most of them. Borrowers will “continue to work with the same loan servicer and repay their loans the same way,” according to official guidance. No action is required from borrowers as the change takes effect.

Treasury student loans takeover 2026: But that reassurance comes with a significant caveat: the system these borrowers are relying on has already been significantly weakened. The Government Accountability Office recently found that the Federal Student Aid office — gutted by layoffs, with roughly half its workforce gone — stopped assessing loan servicers on customer service quality in February 2025, simply because it lacked the staff to do so. Four of five loan servicers were already failing to meet performance standards for record accuracy.

There are also real backlogs piling up. An estimated 1.5 million FAFSA applications are currently delayed, alongside 65,000 Public Service Loan Forgiveness (PSLF) buyback requests awaiting processing. The hope is that Treasury’s operational muscle will help clear these logjams — but that’s far from guaranteed.

A new repayment plan enters the picture

Alongside the Treasury transfer, borrowers face another major change: the income-driven repayment landscape is being overhauled. Effective July 1, 2026, the new Repayment Assistance Plan (RAP) — created under the One Big Beautiful Bill Act, signed on July 4, 2025 — will replace older income-driven repayment options, including the Biden-era SAVE plan, which was officially killed in court.

RAP’s key features include a $10 minimum monthly payment for borrowers earning $10,000 or less annually, with payments scaling from 1% to 10% of adjusted gross income as income rises. Crucially, if a borrower’s monthly payment doesn’t cover the interest accruing on their loan, the government will apply a subsidy to cover the gap — and guarantee at least $50 toward the principal each month. This is designed to prevent the negative amortization problem that plagued earlier plans, where borrowers could see their balances grow even while making on-time payments.

For borrowers who borrowed Parent PLUS loans before July 1, 2026, there’s a grace period: they can continue under old rules for three more years, or until the student’s program ends.

Has Treasury done this before? A cautionary note

Treasury’s track record with student loan management deserves scrutiny. In 2015, the department ran a pilot program — collecting payments from a sample of borrowers already in default. The results were not encouraging: Treasury’s success rate at recovering payments was lower than that of the private collection agencies already contracted by the Education Department.

Defenders of the current transfer argue that Treasury’s Bureau of the Fiscal Service has grown significantly in capability since then, and that the scale and permanence of this new arrangement is fundamentally different from a limited pilot. Still, the past performance raises legitimate questions about whether a tax-collection-focused agency is best equipped to handle the human complexities of student debt — income-based repayments, forgiveness programs, deferment requests, and appeals.

Education Under Secretary Nicholas Kent has argued the move will introduce “banking logic rather than bureaucratic logic” to the system. That framing, while optimistic, remains untested at this scale.

The political battle beneath the surface

The Treasury transfer is not happening in a vacuum. It is the tenth interagency agreement the Education Department has signed as part of the Trump administration’s broader effort to dismantle the department — an effort the U.S. Supreme Court temporarily greenlit in July 2025, when it permitted mass layoffs and a dramatic downsizing plan to proceed.

Congressional Democrats have pushed back hard. Senator Patty Murray of Washington called the move an “illegal hollowing out” of the department and accused the administration of creating “pointless new red tape” while threatening services students depend on daily. Senator Elizabeth Warren has formally written to Secretary McMahon questioning the legal basis for the transfers under the Economy Act.

On the other side, conservatives — including the Heritage Foundation — have long advocated for moving student loans out of Education, with Project 2025 specifically calling for a new “government corporation” to handle student debt. The Treasury transfer is a partial fulfillment of that vision.

What borrowers should do right now

Amid all the institutional upheaval, borrowers have a few practical priorities:

- If you’re in default, expect contact from Treasury-managed collection processes. Look into rehabilitation options and the new RAP plan before July 1, 2026.

- If you’re on SAVE or another income-driven plan, get current on what’s replacing it. RAP takes over July 1, and your payment amounts may change.

- If you have a PSLF application pending, keep documentation of every payment and employer certification. With backlogs at 65,000 requests, patience — and records — are your best tools.

- If you’re currently repaying without issues, the official guidance is that you should see no change. Monitor your servicer’s communications closely regardless

The Treasury Department’s takeover of the first slice of America’s $1.7 trillion student loan portfolio is historic in scope — a seismic institutional shift that has been decades in the making and is now playing out in real time. Whether it results in the “financial discipline” the administration promises or the “confusion and chaos” critics predict will depend on how carefully the transition is managed and whether Treasury’s operational capabilities can match the complexity of what it is inheriting.

For 42 million borrowers already worn down by years of policy whiplash — from pandemic forbearance to SAVE plan uncertainty to default resumption — the answer cannot come soon enough.